- Last month, the Alerian MLP ETF (AMLP) outperformed the S&P 500 Index by 614 basis points (bps) as the Iran war and the near-closure of the Strait of Hormuz tightened global oil and product balances and increased the value of US export-linked midstream assets. While upstream-heavy energy equities moved more sharply with oil, March was still constructive for midstream as buyers turned to US barrels and products, supporting the pipeline, storage, and export systems AMLP is built to own.

- Oil prices saw a historic increase in March, but it is important to note that the oil futures curve broadly lifted. Expectations for higher oil prices in the medium-term has particular benefits for some of the names in AMLP focused on handling crude. For example, Plains All American (PAA, 12.47% weight*) was the best-performer in the portfolio for the month, returning 6.79%. Plains has an extensive Permian footprint, and a higher oil price likely supports a stronger outlook for Permian oil production, particularly into 2027. This was also a tailwind for Enterprise Products Partners (EPD, 12.25% weight*) given its Permian asset base.

Exports of natural gas liquids (NGL) have also been interrupted by the conflict in Iran. EPD and Energy Transfer (ET, 12.31% weight*) currently operate NGL export capacity and have been expanding their capacity. Going forward, the U.S. may be a more preferred supplier to international buyers given its affordable and reliable supply of NGLs. ET rose 2.44% for the month. - Cheniere Energy Partners LP (CQP, 4.69% weight*), which liquefies natural gas for export, gained 5.43% for the month. CQP's volumes of liquefied natural gas (LNG) are largely sold under long-term contracts, limiting exposure to the spike in global LNG benchmarks seen in March. That said, the disruption to LNG flows through the Strait of Hormuz and damage to a Qatari LNG export facility likely make US LNG exports more attractive for international buyers going forward and may support future capacity expansions for LNG facilities. Additional LNG export capacity creates opportunities across the midstream value chain, from gathering wells to processing facilities to large natural gas pipelines that help supply liquefaction plants.

“The situation in the Middle East shows the need for diversity in energy supplies.”

– Jack Fusco, CEO, Cheniere Energy (March 23, 2026)

Why March’s Supply Shock Strengthened the Case for AMLP

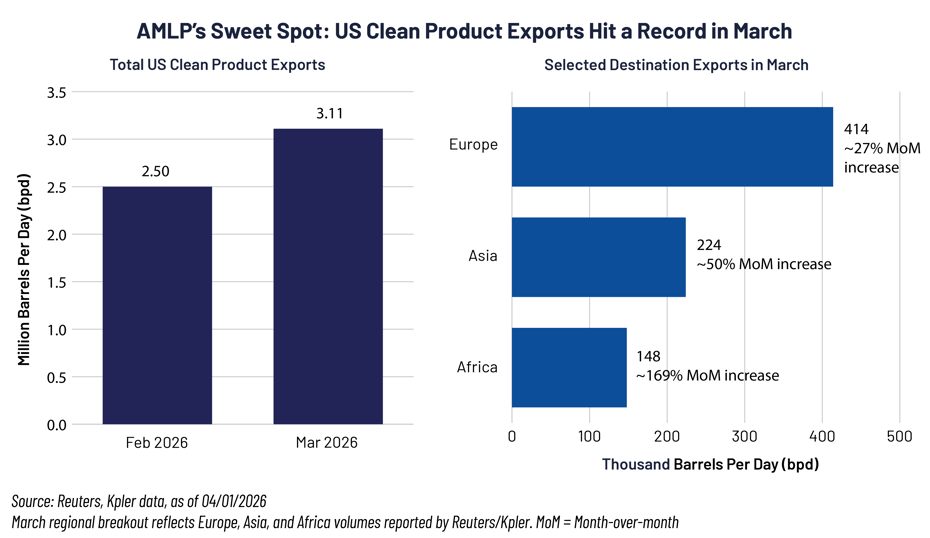

March’s geopolitical shock did more than lift crude prices; it rerouted global trade toward the United States. As the Iran war disrupted traffic through the Strait of Hormuz, the output from Organization of the Petroleum Exporting Countries (OPEC) fell to 21.57 million barrels per day (bpd) in March—the lowest since June 2020. At the same time, buyers across Europe, Asia, and Africa turned to US barrels and refined products to help fill supply gaps, pushing US clean petroleum product exports to a record 3.11 million bpd in March, up from roughly 2.5 million bpd in February.

While markets turned to the US for additional energy supply in the short-term, the US likely becomes a more attractive source of energy for global buyers going forward. Several companies in AMLP play a critical role in transporting energy from where it is produced to the coasts for exports or are actively involved in exports, generating a fee for loading hydrocarbons onto ships. Greater demand for US energy in export markets over time would be positive for the volumes handled by midstream companies.

- AMLP is built around fee-based US midstream operators whose cash flows are tied more to volumes, storage, and long-term contracts than to day-to-day swings in oil. In other words, AMLP gives investors more direct exposure to US energy infrastructure and less direct crude-price volatility than the Energy Select Sector SPDR Fund’s (XLE) more producer-heavy mix.

Performance Summary

| Cumulative | Annualized |

||||||||

| 1 M | YTD | 1 Y | 3 Y | 1 Y | 3 Y | 5 Y | 10 Y | SI | |

| AMLP - NAV (Net Asset Value) | 1.00% | 13.77% | 9.77% | 73.49% | 9.77% | 20.16% | 20.82% | 8.22% | 5.56% |

| AMLP - Market Price | 1.04% | 14.02% | 9.74% | 73.74% | 9.74% | 20.22% | 20.79% | 8.25% | 5.57% |

| Alerian MLP Infrastructure Index - TR | 1.26% | 17.16% | 12.88% | 92.10% | 12.88% | 24.31% | 24.73% | 10.52% | 8.15% |

| Alerian MLP Index - TR | 1.02% | 16.86% | 13.92% | 94.00% | 13.92% | 24.72% | 24.89% | 11.03% | 8.12% |

Source: Bloomberg L.P. and SS&C ALPS Advisors, as of 03/31/2026

Performance data quoted represents past performance. Past performance is no guarantee of future results so that shares, when redeemed, may be worth more or less than their original cost. The investment return and principal value will fluctuate. Current performance may be higher or lower than the performance quoted. For current month-end performance call 1-866-759-5679 or visit www.alpsfunds.com. Performance includes reinvested distributions and capital gains.

Market Price is based on the midpoint of the bid/ask spread at 4 p.m. ET and does not represent the returns an investor would receive if shares were traded at other times.

Fund inception date: 08/24/2010

Total Operating Expenses: 1.01%^

* Weight in AMLP as of 03/31/2026

^ Total Operating Expenses as of 03/31/2026 is comprised of Management Fees of 0.84% and Income Tax Expense of 0.17%. The Fund is classified for federal income tax purposes as a taxable regular corporation or so-called Subchapter “C” corporation. As a “C” corporation, the Fund accrues deferred tax liability for its future tax liability associated with the capital appreciation of its investments and the distributions received by the Fund on equity securities of master limited partnerships considered to be a return of capital and for any net operating gains. The Fund’s accrued deferred tax liability, if any, is reflected each day in the Fund’s net asset value per share. The deferred income tax expense/(benefit) represents an estimate of the Fund’s potential tax expense/(benefit) if it were to recognize the unrealized gains/(losses) in the portfolio. An estimate of deferred income tax expense/(benefit) is dependent upon the Fund’s net investment income/(loss) and realized and unrealized gains/(losses) on investments and such expenses may vary greatly from year to year and from day to day depending on the nature of the Fund’s investments, the performance of those investments and general market conditions. Therefore, any estimate of deferred income tax expense/(benefit) cannot be reliably predicted from year to year.

Top 10 Holdings

| Plains All American Pipeline LP | 12.47% | MPLX LP | 11.58% | |

| Energy Transfer LP | 12.31% | Hess Midstream LP | 9.05% | |

| Enterprise Products Partners LP | 12.25% | Cheniere Energy Partners LP | 4.69% | |

| Sunoco LP | 12.24% | USA Compression Partners LP | 3.95% | |

| Western Midstream Partners LP | 11.99% | Genesis Energy LP | 3.50% |

As of 03/31/2026, subject to change

Important Disclosures & Definitions

An investor should consider the investment objectives, risks, charges and expenses carefully before investing. To obtain a prospectus containing this and other information, call 1-866-759-5679 or visit www.alpsfunds.com. Read the prospectus carefully before investing.

Shares of ETFs are bought and sold at market price (not NAV) and are not individually redeemable.

Performance data quoted represents past performance. Past performance is no guarantee of future results; current performance may be higher or lower than performance quoted.

All investments are subject to risks, including the loss of money and the possible loss of the entire principal amount invested. Additional information regarding the risks of this investment is available in the prospectus.

Investments in securities of Master Limited Partnerships (MLPs) involve risks that differ from an investment in common stock. MLPs are controlled by their general partners, which generally have conflicts of interest and limited fiduciary duties to the MLP, which may permit the general partner to favor its own interests over the MLPs.

A portion of the benefits you are expected to derive from the Fund’s investment in MLPs depends largely on the MLPs being treated as partnerships for federal income tax purposes. As a partnership, an MLP has no federal income tax liability at the entity level. Therefore, treatment of one or more MLPs as a corporation for federal income tax purposes could affect the Fund’s ability to meet its investment objective and would reduce the amount of cash available to pay or distribute to you. Legislative, judicial, or administrative changes and differing interpretations, possibly on a retroactive basis, could negatively impact the value of an investment in MLPs and therefore the value of your investment in the Fund.

The Fund invests primarily in a particular sector and could experience greater volatility than a fund investing in a broader range of industries.

Investments in the energy infrastructure sector are subject to: reduced volumes of natural gas or other energy commodities available for transporting, processing or storing; changes in the regulatory environment; extreme weather and; rising interest rates which could result in a higher cost of capital and drive investors into other investment opportunities.

The Fund employs a “passive management” - or indexing - investment approach and seeks investment results that correspond (before fees and expenses) generally to the performance of its underlying index. Unlike many investment companies, the Fund is not “actively” managed. Therefore, it would not necessarily sell or buy a security unless that security is removed from or added to the underlying index, respectively.

Alerian MLP Index (AMZ): the leading gauge of energy infrastructure MLPs. The capped, float-adjusted, capitalization-weighted index constituents earn the majority of their cash flow from midstream activities involving energy commodities.

Alerian MLP Infrastructure Index (AMZI): a composite of energy infrastructure Master Limited Partnerships (MLPs). The capped, float-adjusted, capitalization-weighted index constituents earn the majority of their cash flow from midstream activities involving energy commodities.

Basis Point (bps): a unit that is equal to 1/100th of 1% and is used to denote the change in a financial instrument.

Master Limited Partnership (MLP): a business venture that exists in the form of a publicly traded limited partnership. They combine the tax benefits of a private partnership - profits are taxed only when investors receive distributions - with the liquidity of a publicly traded company.

Tailwind: a certain situation or condition that may lead to higher profits, revenue or growth.

One may not invest directly in an index.

ALPS Advisors, Inc., registered investment adviser with the SEC, is the investment adviser to the Fund. ALPS Advisors, Inc. and ALPS Portfolio Solutions Distributor, Inc., affiliated entities, are unaffiliated with VettaFi and the Alerian Index Series.

ALPS Portfolio Solutions Distributor, Inc. is the distributor for the Fund.

Not FDIC Insured • No Bank Guarantee • May Lose Value

ALR002066 07/31/2026